The income tax department, on 2 June has released Income Tax Return(ITR) 1-SAHAJ with a few changes in the structure itself. First of all, we will look at the category of persons required to file ITR-1 SAHAJ. It is filed by an individual being a resident (other than not ordinarily resident) having total income up to Rs.50 lakh, having Income from Salaries, one house property, other sources (Interest etc), and agricultural income up to Rs. 5000. Additionally, in the ITR-1 released for AY 2020-21 three categories of persons are also included.

- Individuals who have deposited an amount or aggregate of amounts exceeding Rs. 1 Crore in one or more current account during the previous year.

- Individuals who have incurred an expenditure of an amount or aggregate of the amount exceeding Rs. 2 lakhs for travel to a foreign country for yourself or for any other person.

- Individuals who have incurred an expenditure of amount or aggregate of an amount exceeding Rs. 1 lakh on the consumption of electricity during the previous year.

Filing ITR-1 is not a difficult task at all. It requires a little bit of precision and understanding of the utility. The utility contains spaces for information such as TAN of employer, Salary under the different sub-section of section 17 and deductions availed, which is provided in the form 16 Part B by the employer itself. But there are a few things one should keep in mind while filing ITR-1.

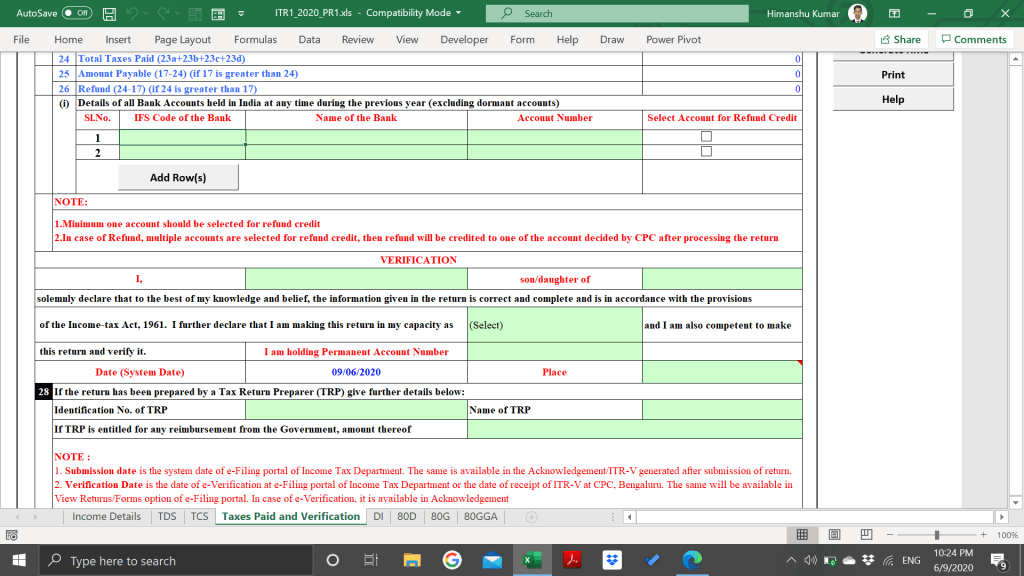

- Fill valid bank details and enter verification details. It is one of the common mistakes observed, when the ITR is filed by a common man. Without bank and verification details the utility will not generate a XML file. The bank details will also be required to confirm the bank account in which assessee want income tax refund (if any), in case assessee hold more than one bank account.

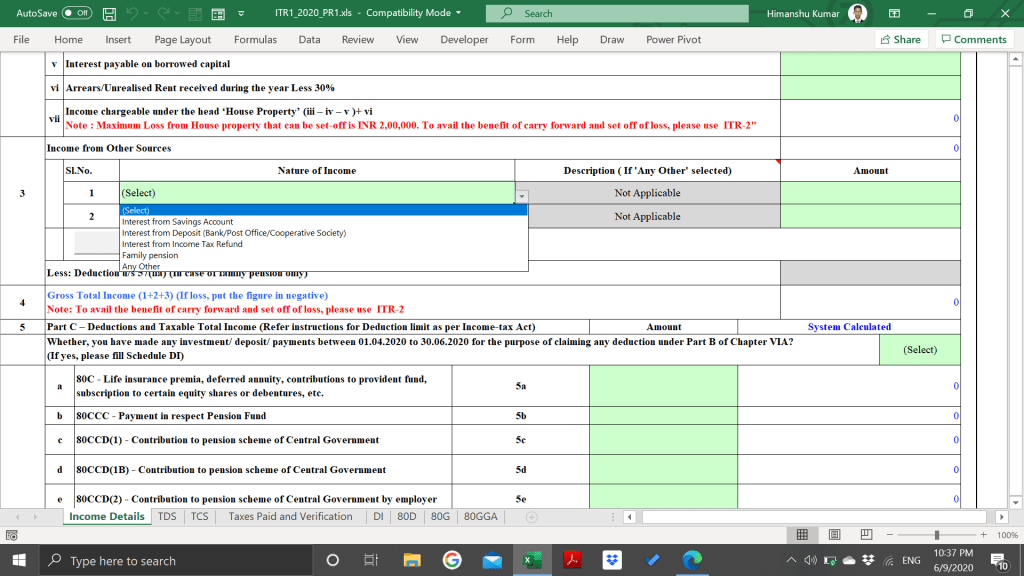

- Declaring income under the head other sources. Income as interest from saving bank account, deposits and income tax refund is also a part of Gross total income and individuals often tends to leave that part blank.

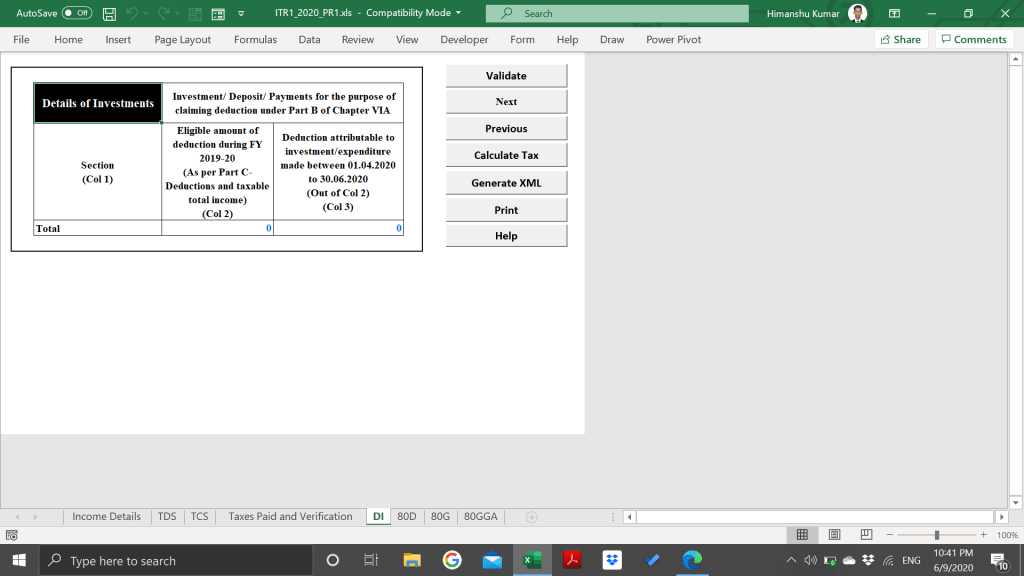

- Claiming deductions under proper period. As a part of COVID-19 relief, investment made after 31 March, 2020 up to 30 June, 2020 is also admissible to be claim as deduction. But for that purpose assessee needs to declare in the return itself about the part of investment made in that period.

If you feel any difficulty in filling your return please let me know in the comment section below. We’ll get back to you within 2 days of raising query.